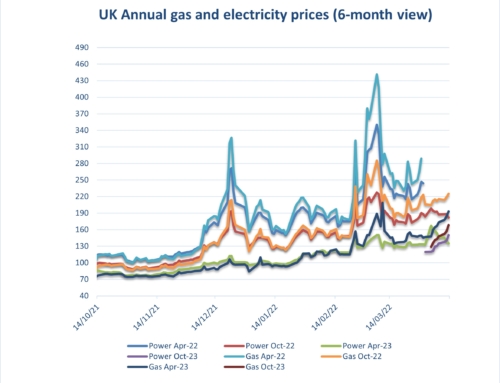

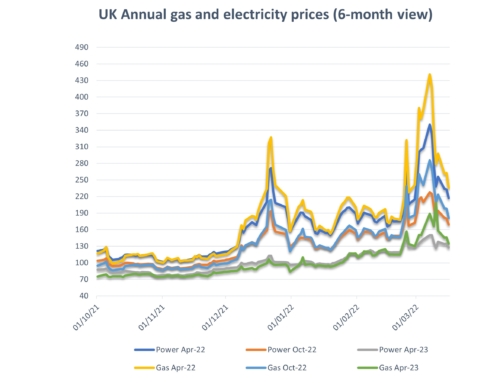

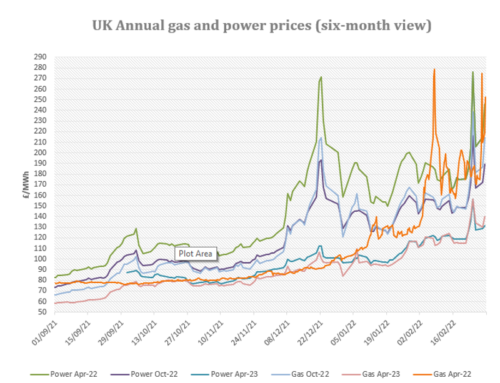

Energy costs: Choppy market conditions continued in late June, fuelled by a tug of war between oil price volatility, changeable weather and rising CO2 costs. Although the overall trend was marginally downwards, however it still has not reached March/April lows. This volatile dynamic is likely to continue as OPEC look set to extend current oil production cuts to the end of 2019, while temperatures (which have settled in the last few days) are predicted to increase again.

Upside:

Gas maintenance – Unplanned outages Norwegian gas field with no definite end date in sight continue.

LNG deliveries– LNG shipments continue to head towards Europe although at a slower rate.

Oil prices – Oil prices have increased ahead of the likely extension of production cuts by OPEC and continued tensions in the Gulf.

Coal markets – Coal prices have rebounded due to the beginning of the summer maintenance period.

Carbon (CO2) markets – Prices remain buoyant and look likely to continue that way.

Downside:

Gas storage – Storage levels remain healthy for this time of year.

Wind/solar output – Strong solar and wind generation is predicted for the first half of July.

Could go either way:

Brexit/Sterling – No change here, with little prospect of an agreement in the short-term this continues to be an area of significant risk. If the UK crashes out, Sterling may devalue further amplifying any increases in feeder markets.

Non-energy costs: On the electricity side organisations will see further increases in pass through costs from both government and industry infrastructure providers in the coming months as distribution, Electricity Market Reform (EMR),Capacity Market and Energy Intensive Industries (EII) charges are ramped up.

Climate change levy (CCL) increased significantly from April 1st to offset the loss of CRC to Government revenues. Please see the attached pass through charge information for details. Your CCA related CCL exemption rates will increase at the same time (Gas 78%, Electricity 93%). Please ensure your PP11 forms are updated and sent through.

Warning: more gas suppliers are passing through backdated Un-identified Gas (UIG) charges for 2017/18. Please contact us if you have any questions or unusual gas bills.

Are you eligible for an EII rebate?

In August, the Government announced a consultation to extend the existing scheme which will be concluded shortly. Under current rules, if you qualify at an industry sector level and your business passes the 20% electricity intensity test you may qualify for exemption to CFD and RO charges. Please see the attached Government RO/CFD guidance document and give me a call to discuss this further. We will keep you updated with any confirmed changes to the scheme likely to feed through in the next month.

A copy of our detailed market report is available: Eneco Market Information early July 2019

Gas and electricity prices from 2009 to date are available here: Eneco Gas and Electricity Pricing Trends Sept 2009 to early July 2019

A copy of our environmental charges and Climate Change Levy rates from 2012 to date: Environmental Pass Through Charges and CCL ppkWh Updated 15.04.19

A copy of RO/CFD guidance document: RO_CFD_Guidance_Revised_July_2018

{kind=link}

{kind=link}