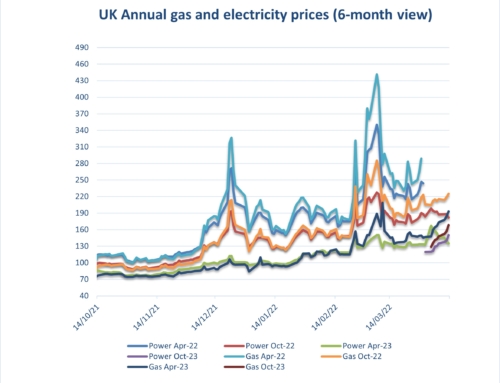

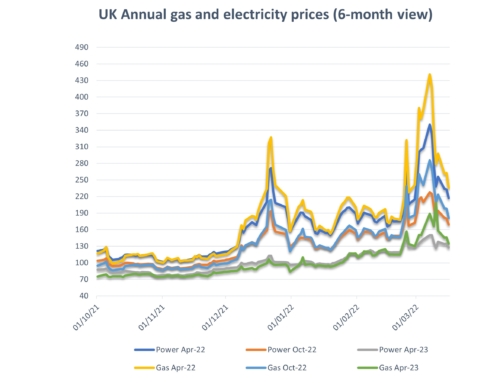

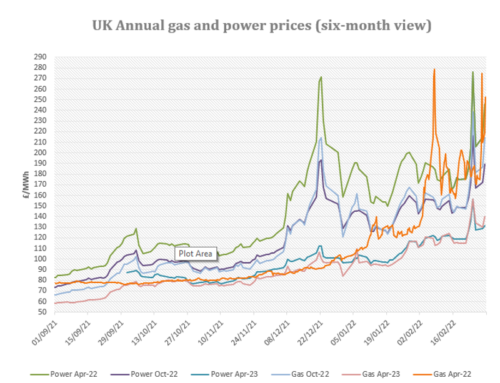

Energy costs: Short term energy prices have been volatile over the second half of September following fluctuating wind generation between 1% and 45%, falling LNG imports and increase in coal prices due to increased European coal burning, industrial action in Columbia and South Africa and fears of La Nina weather disruptions into Winter. On top of this, a fire at a Norwegian Hammerfest LNG plant which is going to be out of action for at least one month has pushed prices up as well as Covid-19 flare up affecting economic outlook. Long term prices have reduced as various plants finish maintenance with a strong supply outlook, bearish EUAs, and further injections into European storage sites.

Upside:

Reduced Production – Holland’s Groningen field (Europe’s biggest producing field) is being wound down as withdrawing gas from the site causes earthquakes.

Oil markets – Oil markets have been volatile from falling US inventories counteracted by a ramp up from Libya and Iran. However, strikes in Norway will affect prices.

LNG – Falling LNG imports and fire at Norwegian plant causing this to be shut for at least a month.

Strike Action – Norwegian offshore workers strike to reduce oil and gas output by 22%.

Weather – Temperatures predicted to remain below seasonal norm and fears over La Nina weather forming as we move closer to Winter. This would increase the overall gas demand and push coal prices up if heavy rain and flooding disrupts key coal-producing nations.

Wind output – Expected to drop due to the jet-stream moving to the South. However, RWE will be extending four offshore wind farms in the UK to help with renewable wind generation.

Downside:

Gas storage – European gas storage has been replenished which is now at 95% fullness.

UK Power Capacity – 4GW of gas-fired UK power capacity due to come onstream this month.

EUAs – This is expected to reduce throughout the remainder of the year by a record 17%

Could Go Either Way:

Sterling – Brexit negotiations have returned to the news. Problems in this area will feed through to exchange rates and impact energy prices.

Lockdown – If further lockdowns in the UK and globally are announced, it will intensify economic fears but would reduce energy demand.

Non-energy costs:

On the electricity side organisations will see further increases in pass through costs from both government and industry infrastructure providers in the coming months as the Targeted Charging Review (TCR) is added to the other distribution, transmission, Electricity Market Reform (EMR), Capacity Market, Energy Intensive Industries (EII) charges already in place.

Climate change levy (CCL) again changed on April 1st. Your CCA related CCL exemption rates changed at the same time (Gas to 81%, Electricity to 92%). Please ensure your PP11 forms are updated and sent through.

Is your organisation covered by the new Streamlined Energy and Carbon Reporting (SECR) scheme?

Designed to replace in part the Carbon Reduction Commitment (CRC) which ends this year and to follow on from the energy savings recommendations generated by ESOS compliance. Note, SECR will cover a wider scope of organisations than CRC and ESOS do. Full details are attached below.

SECR will require all large enterprises to disclose within their annual financial filing obligations to Companies House, their greenhouse gas emissions, energy usage (from gas, electricity and transportation as a minimum), energy efficiency actions and progress against at least one intensity ratio.

The scheme came into effect on April 1st, 2019 and will be required to be included in the first set of accounts published for financial years starting after this date.

The scheme covers publicly quoted companies (extending their current disclosure requirements) and UK incorporated companies or LLPs with two or more of the following.

- More than 250 employees

- A turnover in excess of £36 million

- A balance sheet in excess of £18 million.

UK subsidiaries, who meet the eligibility criteria, but are covered by a parent group’s report (unless the parent group is registered outside the UK) and companies using less than 40,000 kWh of energy during the reporting year do not have to provide disclosure. Note the reporting year should be aligned to your financial year.

Are you eligible for an EII rebate?

Under current rules, if you qualify at an industry sector level and your business passes the 20% electricity intensity test you may qualify for exemption to CFD and RO charges. Please see the attached Government RO/CFD guidance document and update and give Abby a call on the main number to discuss this further.

A copy of our detailed market report is available: Eneco Market Information early October 2020

Gas and electricity prices from 2009 to date are available here: Eneco Gas and Electricity Pricing Trends Sept 2009 to early Oct 2020

A copy of our environmental charges and Climate Change Levy rates from 2012 to date: Environmental Pass Through Charges and CCL ppkWh Updated 21.07.20

A copy of RO/CFD guidance document: RO_CFD_Guidance_Revised_July_2018

SECR: SECR EA Guidelines

TCR Charges (Targeted Charging Review): TCR Charges (Targeted Charging Review)

{kind=link}