Eneco market reports early June 2021

Energy costs:

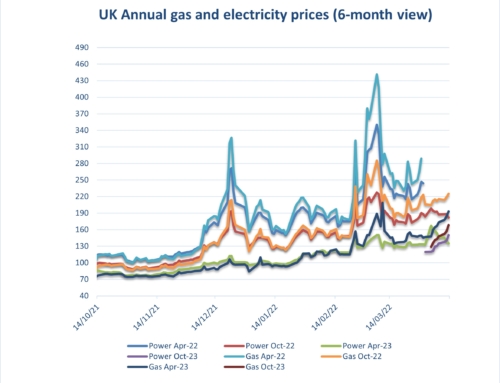

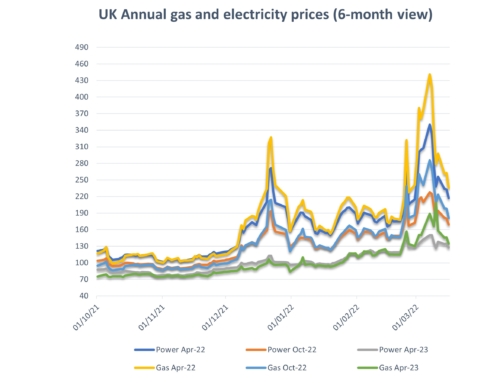

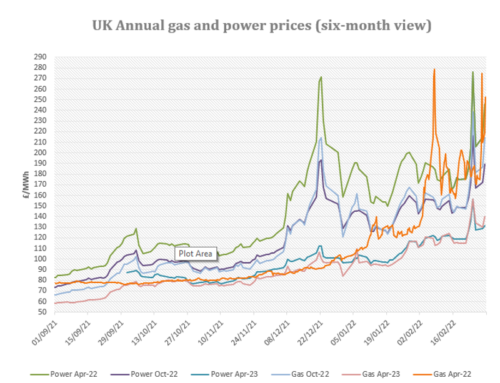

In the last fortnight annuals energy markets have swung by over 10% and short term markets by up to 50% as extreme volatility continued.

Supply concerns persist with Norwegian gas maintenance expected to continue to June 24th, problems between Russia and Ukraine again threatening supplies, and limited LNG deliveries with cargoes diverted to higher prices in the Far-East.

Oil markets continue to gain breaching $70/barrel with OPEC sticking to its stepped relaxation of production cuts and fuel demand increasing globally as the Covid vaccine rollout continues. Coal reached $82/tonne, with strike-related production outages in Colombia and increased Chinese buying.

Higher temperatures in the UK although reducing domestic demand have not reversed recent gains yet, especially since windless conditions have kept gas demand for power generation high. The prolonged cold snap in May has prevented injections into gas storage across Europe and it is now thought these will not be filled before Winter begins.

There is some hope on the horizon with warmer temperatures expected to persist for a while, Iranian oil exports likely to re-commence later on in the year, and the Nordstream-2 pipeline between Russia and Germany finally set to complete at the end of the year.

Upside:

Supply outages –Norwegian gas production outages are likely to continue until June 24th. Russian gas exports are again at risk due to further arguments with Ukraine.

Oil markets – Oil has risen above $70/barrel as global fuel demand increases. Iranian oil exports are expected to re-commence later this year.

Gas storage – European storage is at 37%, compared to 74% this time last year. European storage is not expected to be full by Winter.

Coal – Prices reached $82/tonne, with reduced supply and increased demand.

LNG – LNG deliveries are being diverted by strong buying and higher prices on Asian markets

Vaccine rollout – UK lockdown measures continue to be eased with the successful vaccine rollout, boosting demand and economic confidence.

Downside:

Weather – Warmer temperatures across the UK have diminished gas demand.

Carbon costs – EUETS has fallen back slightly to Euro 54/TC02. The UK’s scheme (UKETS) is now up and running.

Nordstream 2 – This is now due for completion at the end of the year, following the US dropping its sanctions.

Could go either way:

Sterling – has continued to strengthen against both the Dollar and Euro shielding the UK energy markets for some of the impact of oil, coal and carbon price increases. The continued rollout of the UK’s vaccination programme will influence its future direction.

Non-energy costs:

On the electricity side organisations will see further increases in pass through costs from both government and industry infrastructure providers from 2022 onwards due to pandemic-related demand destruction. Levies normally collected via unit rates have fallen short of expectations and have fed through to further increases in ROs, FiTs, EII and other transportation, distribution and renewable investment charges. Targeted Charging Review will now take affect from April 1st 2022, one year later than expected, but are now being built into longer term contracts. Revised projections are available on our website via the links below.

Is your organisation covered by the new Streamlined Energy and Carbon Reporting (SECR) scheme from the Environment Agency?

Designed to replace in part the Carbon Reduction Commitment (CRC) which ended in 2019 and to follow on from the energy savings recommendations generated by ESOS compliance. Note, SECR will cover a wider scope of organisations than CRC and ESOS do. SECR requires all large enterprises to disclose within their annual financial filing obligations to Companies House, their greenhouse gas emissions, energy usage (from gas, electricity and transportation as a minimum), energy efficiency actions and progress against at least one intensity ratio.

If your organisation qualifies, participation in this scheme is mandatory. Eneco Consulting are happy to provide assistance with your regulatory obligations. Full details are available on our website on the link below.

Are you eligible for an EII rebate?

Under current rules, if you qualify at an industry sector level and your business passes the 20% electricity intensity test you may qualify for exemption to CFD and RO charges. Please see the attached Government RO/CFD guidance document and update and give Abby a call on the main number to discuss this further.

Eneco market information early June 2021

Gas and electricity prices from 2009 to date

A copy of our environmental charges and Climate Change Levy rates from 2012 to date: Environmental Pass Through Charges and CCL with Definitions ppkWh 02.12.20

A copy of RO/CFD guidance document: RO_CFD_Guidance_Revised_July_2018

SECR: SECR EA Guidelines

TCR Charges (Targeted Charging Review this will be revised shortly): TCR Charges (Targeted Charging Review)

{kind=link}