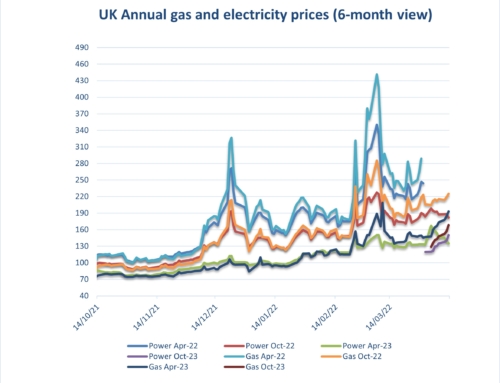

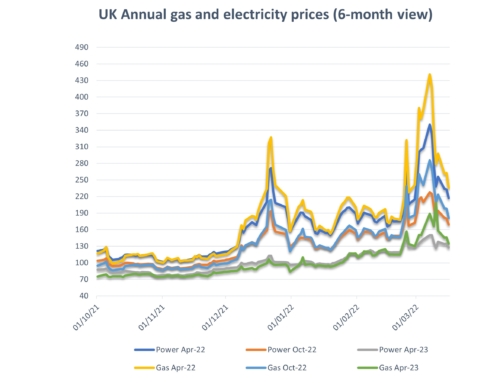

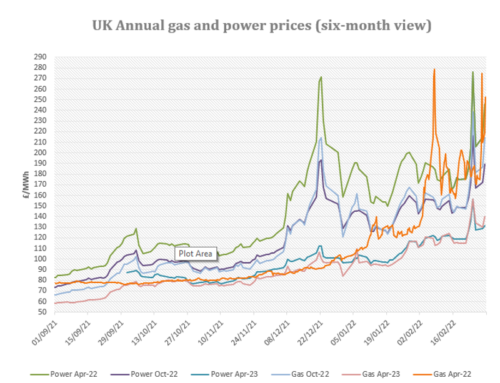

Energy costs:

The last fortnight has been a tale of two halves. The markets rose in the first half due to increases across the broader energy spectrum caused by Hurricanes in the Gulf of Mexico, industrial action across Norwegian oil and gas fields and beyond, maintenance outages (both planned and unplanned) and colder weather. Towards the end of October as a second wave of lockdowns were announced across Europe, many expected to last until the end of November, prices fell back again. However, although the impact of these continued lockdowns is likely to suppress prices for the near future and National Grid are confident of the Winter supply outlook, there are a few supply concerns. Both increasing prices for LNG in Asia attracting supplies away from Europe and outages related to Covid delayed maintenance remain problematic.

Upside:

Supply Outages – Hammerfest gas plant in Norway is to remain shut until the end of while damage assessments and repairs are carried out following the fire that took place last month.

LNG – Increasing demand and prices in Asia is attracting supplies away from Europe.

Weather – Weather is likely to be unsettled for the coming fortnight with low wind generation and decreasing temperatures.

Downside:

Gas storage – European gas storage has remained stable at 95% fullness.

Carbon Costs – These prices have slipped by 8% over the last fortnight, partly on concerns about the impact of a no-deal Brexit and partly because of lockdowns.

Oil markets – Oil markets have shed 12% of value. Although OPEC are discussing further supply cuts which may correct this.

Lockdown – As lockdown has commenced, demand is unlikely to be impacted as much compared to the first lockdown. However, it is likely to keep a lid on significant price increases.

Could go either way:

Sterling – Brexit negotiations are ongoing and predictions of a no-deal. Any problems in this area will feed through to exchange rates and impact energy prices and also are impacting carbon costs.

Non-energy costs:

On the electricity side organisations will see further increases in pass through costs from both government and industry infrastructure providers in the coming months as the Targeted Charging Review (TCR) is added to the other distribution, transmission, Electricity Market Reform (EMR), Capacity Market, Energy Intensive Industries (EII) charges already in place.

Climate change levy (CCL) again changed on April 1st. Your CCA related CCL exemption rates changed at the same time (Gas to 81%, Electricity to 92%). Please ensure your PP11 forms are updated and sent through.

Is your organisation covered by the new Streamlined Energy and Carbon Reporting (SECR) scheme?

Designed to replace in part the Carbon Reduction Commitment (CRC) which ends this year and to follow on from the energy savings recommendations generated by ESOS compliance. Note, SECR will cover a wider scope of organisations than CRC and ESOS do. Full details are attached below.

SECR will require all large enterprises to disclose within their annual financial filing obligations to Companies House, their greenhouse gas emissions, energy usage (from gas, electricity and transportation as a minimum), energy efficiency actions and progress against at least one intensity ratio.

The scheme came into effect on April 1st, 2019 and will be required to be included in the first set of accounts published for financial years starting after this date.

The scheme covers publicly quoted companies (extending their current disclosure requirements) and UK incorporated companies or LLPs with two or more of the following.

- More than 250 employees

- A turnover in excess of £36 million

- A balance sheet in excess of £18 million.

UK subsidiaries, who meet the eligibility criteria, but are covered by a parent group’s report (unless the parent group is registered outside the UK) and companies using less than 40,000 kWh of energy during the reporting year do not have to provide disclosure. Note the reporting year should be aligned to your financial year.

Are you eligible for an EII rebate?

Under current rules, if you qualify at an industry sector level and your business passes the 20% electricity intensity test you may qualify for exemption to CFD and RO charges. Please see the attached Government RO/CFD guidance document and update and give Abby a call on the main number to discuss this further.

A copy of our detailed market report is available: Eneco Market Information early November 2020

Gas and electricity prices from 2009 to date are available here: Eneco Gas and Electricity Pricing Trends early Nov 2020

A copy of our environmental charges and Climate Change Levy rates from 2012 to date: Environmental Pass Through Charges and CCL ppkWh Updated 21.07.20

A copy of RO/CFD guidance document: RO_CFD_Guidance_Revised_July_2018

SECR: SECR EA Guidelines

TCR Charges (Targeted Charging Review): TCR Charges (Targeted Charging Review)

{kind=link}