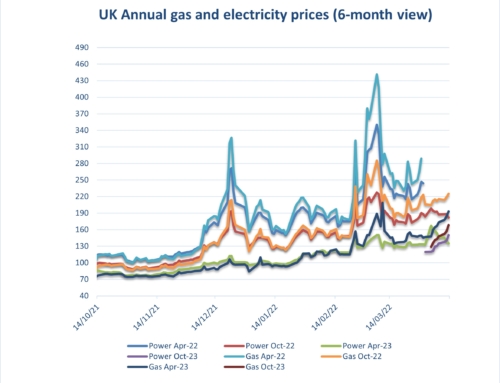

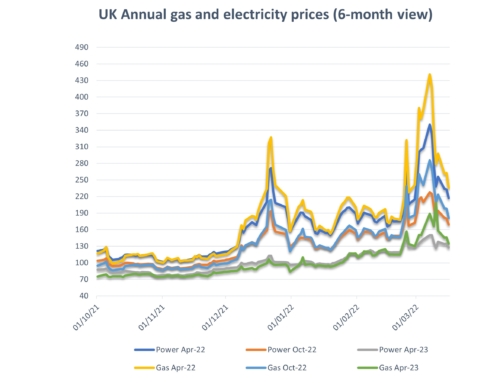

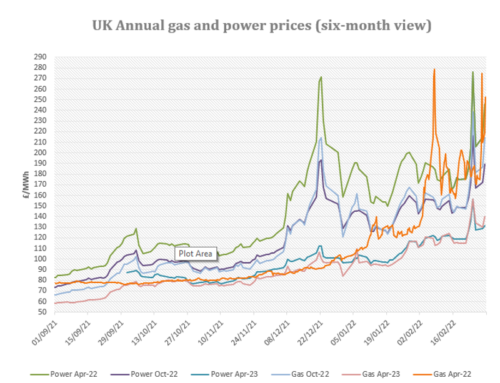

Energy costs: Gas and electricity markets ticked upwards in early October following oil and coal markets. This was driven by increased Middle Eastern tensions following a missile attack on an Iranian oil tanker and concerns regarding coal supply capacity and increasing environmental compliance costs. Subsequently gas and electricity prices fell back, amid hopes of a resolution to Brexit, a strengthening pound and declarations from National Grid of no expected capacity issues this winter following the UK’s departure. Any further increases over the coming fortnight are likely to be stemmed by strong LNG deliveries (with at least 13 expected in October) as tankers reroute to the UK with European stores full.

Upside:

Maintenance –Outages are always a possibility at this time of year.

Coal/Oil markets – Prices have been volatile over the last fortnight. This is likely to continue if tensions in the Middle East continue to ramp up.

Downside:

Gas storage – 98% across Europe, significantly higher than this time last year.

LNG deliveries– At least 13 LNG shipments are expected to arrive in the UK by the end of the month.

Wind output – Wind generation is expected to remain high over the coming fortnight.

Temperatures – Forecasters are predicting temperatures above seasonal norm throughout October.

Could go either way:

Brexit/Sterling – Until an agreement is reached over Brexit, this will remain an area of significant risk. If the UK crashes out, Sterling devaluation will amplify any increases in fuel markets.

Carbon (CO2) markets – Prices have remained below recent resistance levels since the beginning of the month. However, we did see a big hike in prices at the end of April, when a no-deal Brexit previously seemed imminent.

Non-energy costs: On the electricity side organisations will see further increases in pass through costs from both government and industry infrastructure providers in the coming months as distribution, Electricity Market Reform (EMR),Capacity Market and Energy Intensive Industries (EII) charges are ramped up.

Climate change levy (CCL) increased significantly from April 1st to offset the loss of CRC to Government revenues. Please see the attached pass through charge information for details. Your CCA related CCL exemption rates will increase at the same time (Gas 78%, Electricity 93%). Please ensure your PP11 forms are updated and sent through.

Warning: more gas suppliers are passing through backdated Un-identified Gas (UIG) charges for 2017/18. Please contact us if you have any questions or unusual gas bills.

Is your organisation covered by the new Streamlined Energy and Carbon Reporting (SECR) scheme?

Designed to replace in part the Carbon Reduction Commitment (CRC) which ends this year. However, SECR will cover a wider scope of organisations than CRC did. Full details are attached below.

Are you eligible for an EII rebate?

Under current rules, if you qualify at an industry sector level and your business passes the 20% electricity intensity test you may qualify for exemption to CFD and RO charges. Please see the attached Government RO/CFD guidance document and give me a call to discuss this further.

A copy of our detailed market report is available: Eneco Market Information mid October 2019

Gas and electricity prices from 2009 to date are available here: Eneco Gas and Electricity Pricing Trends Sept 2009 to mid Oct 2019

A copy of our environmental charges and Climate Change Levy rates from 2012 to date: Environmental Pass Through Charges and CCL ppkWh Updated 04.01.19

A copy of RO/CFD guidance document: RO_CFD_Guidance_Revised_July_2018

{kind=link}